Materiality analysis is the compass of our journey towards sustainable business transformation. It helps to sharpen the priorities related to ESG factors, i.e. environmental, social and good governance of organizations, on which to focus our strategies and actions to protect the Group's ability to create lasting value.

Since 2014, we have been conducting a process of materiality assessment at least every three years. In 2019, we developed the materiality analysis process methodology by concentrating our efforts on the identification of the mega trends, i.e., the large social, environmental and governance transformations, which is expected to be able to change the world of enterprises, society and the natural environment significantly over a ten-year horizon, and this entails risks and opportunities for Generali, its value chain and its stakeholders.

During 2020, following the COVID-19 pandemic, we reviewed the relevance of the materiality analysis conducted the previous year and we confirmed its validity, making limited changes because we believe that the priorities previously identified still constitute an effective summary of the main business and social challenges for the years to come. The Board of Directors approved these updates in November 2020 and the distribution of the priorities of our sustainable transformation within three priority clusters that determine the Group’s approach to their management.

In 2022, such analysis continued to guide the Group’s approach to managing and reporting on megatrends, also in light of the perspective of the potential impact that they can have on the Group and how they can be influenced by the Group, also through its value chain. Belonging to one of the three priority clusters determines the Group’s approach to its management and reporting.

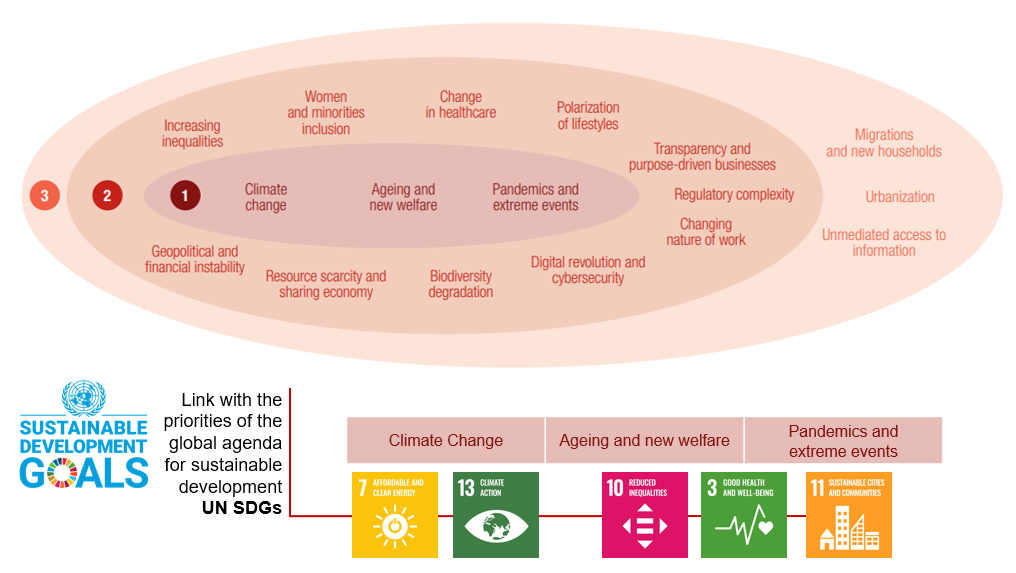

The priorities outlined are placed at the heart of our strategies to generate lasting value for all stakeholders and are clearly anchored in the UN 2030 Agenda and the related Sustainable Development Goals (SDGs):

- climate change is linked with SDG number 7 “affordable and clean energy” and 13 “climate action”

- ageing and new welfare is linked with number 3 “good health and well-being” and 10 “reduced inequalities”

- pandemics and extreme events is linked with number 3 “good health and well-being” and 11 “sustainable cities and communities”

Climate change

Mega trend material to the Group's strategy and considering stakeholders’ expectations; it refers to global warming due to the emissions rise of greenhouse gases coming from human activities, which is intensifying extreme natural events such as floods, storms, rise in sea level, drought, wildfire and heat waves, with repercussions on the natural ecosystems, human health and the availability of water resources. The policies and efforts required to limit global warming to below 1.5°C through the decarbonisation of the economy will lead to radical changes in the production and energy systems, transforming especially carbon-intensive activities, sectors and countries and encouraging the development of clean technologies. As effective as these efforts may be, some changes will be inevitable, therefore making strategies to adapt and to reduce the vulnerability to the changing climate conditions necessary.

Ageing and new welfare

Mega trend material to the Group's strategy and considering stakeholders’ expectations; it refers to trend of increasing life expectation and reducing birth rates that will make sizeable impacts on the financial sustainability of the social protection systems and might lead to reduced public welfare services. The aging of the population will also influence the job market and consumption, with effects on productivity and the intergenerational relations, with increased welfare costs borne by the working population.

Pandemics and extreme events

Mega trend material to the Group's strategy and considering stakeholders’ expectations; it refers to the fact that the population concentration and the deficiencies in population protection and emergency management mechanisms are increasing the risks associated with extreme events, such as earthquakes and tsunamis, pandemics and health emergencies as well as other man-made catastrophes such as technological, radiological incidents, and terrorism. A strengthening of the system to prevent, prepare for and respond to these events is required in order to increase the resilience of the affected territories and communities.

Geopolitical and financial instability

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the weakening of multilateralism and of the traditional global governance mechanism that are leading to increased tension between countries and to the resurgence of trade protectionism and populism. Associated with the changing geopolitical balance - with complex cause and effect relationships - is the worsening of macroeconomic conditions and a scenario of a continuing lowering of interest rates. The weakening of the initiative of the traditional political institutions is compensated by the emergence of coalitions and global coordination mechanisms promoted by the private sector and civilian society.

Increasing inequalities

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the growing gap in the distribution of wealth between social groups and - more in general - the polarisation in accessing self-determination opportunities. These trends are accompanied with a decline in social mobility, leading to a protracted permanence in the state of poverty and exclusion, mainly related to the socio-economic conditions of the household of origin.

Women and minorities inclusion

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the growing demands for greater inclusion and empowerment of the diversities related to gender, ethnic group, age, religious belief, sexual orientation and disability conditions in the various areas of social life, from the workplace to that of political representation and public communication. The topic of women empowerment and reducing the gender pay and employment gaps has taken on particular emphasis. However, in the face of these trends an increase in forms of intolerance, social exclusion and violence is noted, particularly against women, ethnic and religious minorities, immigrants and LGBTI+ people and those with mental-physical disabilities, especially in the lower income and lower education social brackets.

Change in healthcare

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the transformation of the healthcare systems due to demographic, technological and public policy evolution, leading to a higher demand for increasingly advanced patient-centric healthcare services, with growing healing and quality treatment expectations. That means that the level of sophistication and of healthcare service cost is growing, with an increasing integration of the public offer with private sector initiative.

Polarization of lifestyles

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the enhanced awareness of the connection between health, living habits and the environmental, which is favouring the spread of healthier lifestyles, based on the prevention and proactive promotion of well-being, especially in the higher income and higher education social groups. Examples of this are the growing attention to healthy eating and to physical activity. However, amongst the more vulnerable social brackets, unhealthy lifestyles and behaviours at risk are continuing, if not actually increasing, with the spread of different forms of addiction (drugs, alcohol, tobacco, compulsive gambling, Internet and smartphone addiction), mental discomfort, sleep disorders, incorrect eating habits and sedentariness, with high human and social costs related to healthcare expenditure, loss of production and early mortality.

Transparency and purpose-driven businesses

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the fact that key stakeholders of companies - such as investors, consumers and employees, especially in Europe and with particular reference to the Millennial - are ever more attentive and demanding on the purpose and the sustainability practices of companies. Also, the regulatory requirements for companies in terms of reporting and transparency are increasing, making it increasingly essential that a company demonstrate its ability to create value for all of its stakeholders, going beyond the shareholders. The growing number of benefit companies, cooperatives and social enterprises stands as proof of this trend.

Regulatory complexity

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the increase in the production of laws and regulatory mechanisms especially for the financial sector, in order to regulate its complexity and to share the fight against illegal economic activities with the sector’s participants. Therefore, the costs for guaranteeing regulatory compliance and the need for greater integration and simplification of the governance systems are increasing.

Changing nature of work

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the transformation in the labour market due to new technologies, the globalisation and the growth of the service industry which are a leading to the spread of a flatter and more fluid organisation of work, as the diffusion of agile and flexible working arrangements, the job rotation and smart working solutions show. Self-employed workers and freelance collaborations are also on the rise versus a stagnation of employment, which make the labour market less rigid but also more precarious, irregular and discontinuous. In terms of changes in the real economy, the number of SMEs is increasing in Europe and we are witnessing a restructuring of the traditional industrial sectors and the globalization of the production processes with an increased complexity of the supply chains.

Digital revolution and cybersecurity

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the technological innovations introduced by the fourth industrial revolution, including big data, artificial intelligence, the Internet of Things, automation and block chain which are transforming the real economy and the social habits with the spread of services featuring a high level of customization and accessibility. The digital transformation requires new know-how and skills, resulting in a radical change of traditional jobs and in the appearance of new players on the market. The growth in complexity, interdependence and speed of innovation of the new digital technologies are posing challenges associated with the security of IT systems and infrastructures.

Biodiversity degradation

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the rapid extinction of many animal and plant species, with a impoverishment of biological diversity and the gene pool, due to the land conversion, to the increase in pollution levels and to the climate change. The progressive collapse of the natural ecosystems represents a growing risk also for human health as it impairs the food chain, reduces resistance to pathogens and threatens the development of communities and economic sectors that strongly depend on biodiversity, such as farming, fishing, silviculture and tourism. In the face of this threat, the activism of civil society, regulatory pressure and the supervision of the authorities are growing, which broaden the responsibility of companies not only as regards their own operations, but also regarding their supply chain.

Resource scarcity and sharing economy

Mega trend of high relevance to the Group's strategy and considering stakeholders’ expectations; it refers to the increase in world population and the excessive exploitation of natural resources such as soil, land water, raw materials and food resources that make the transition to circular and responsible consumption models necessary as they reduce the resources use and the waste production. Technological innovation and the spread of more sustainable lifestyles encourage the spread of new consumption and production patterns based on reuse and sharing, such as car sharing, co-housing, co-working and crowdfunding.

Migrations and new households

Mega trend monitored by the Group; it refers to the migration phenomena and increased international mobility that are broadening the cultural diversity of the modern globalised societies and are transforming the preferences and market of the consumers, the workplace and the political debate. Also the profile of modern family is profoundly changing with a significant increase in households made up of only one person and in single-parent families due to greater women emancipation, growth in separations, longer life expectation and urbanisation. As a result, consumption habits, the distribution of resources and the social risk mitigation mechanisms are changing, and the vulnerability of the single-person households to situations of hardship - such as loss of employment or disease - is growing.

Unmediated access to information

Mega trend monitored by the Group; it refers to the increasing speed, ease and amount of information shared between people, governments and companies thanks to the diffusion of new communication technologies, social media and web platforms. In this way, knowledge is increasingly accessible, multi-directional, intergenerational and on a global scale, and is transforming how people form opinions and mutually influence each other. The traditional sources of information, such as newspapers, schools, parties and religious institutions, are undergoing a resizing of their role in mediating knowledge, with consequences for control of the reliability of the information circulated and for manipulating public opinion, as evidenced by the fake news phenomenon.

Urbanization

Mega trend monitored by the Group; it refers to the trend of human population concentrating in urban areas. Today over 70% of Europeans live in cities, and the amount should rise to above 80% by the year 2050. At the same time, over the years land consumption to convert natural land into urbanised areas has accelerated. Together with their expansion, the cities find themselves having to take up increasingly urgent challenges, such as social inclusion in the outskirts and the lack of adequate housing, congestion and air pollution. Considerable investments will therefore be necessary for urban regeneration and to modernise infrastructure and mobility systems based on a more sustainable planning.

THE PRIORITIES GUIDING THE SUSTAINABLE TRANSFORMATION OF OUR BUSINESS STEM FROM THE STRUCTURED LISTENING TO STAKEHOLDERS WITHIN AND OUTSIDE THE GROUP:

As a first step, we have identified ESG factors that are potentially relevant to us in relation to our activities, business strategy and the contexts in which we work. We looked for those systemic changes, also referred to as mega trends for brevity, that over the next 10 years can bring significant risks and opportunities for the Group, our value chain and the stakeholders.

We analyzed public documents providing scenario analysis and research on sustainable development policies, issued by international institutions or non-governmental associations, think-tanks, associations and industry forums. We also analyzed key internal documents, such as the Group strategy and the results of the Group's risk assessment process, including emerging risks. We also carried out industry and benchmark analyses, examining material topics identified by large insurance groups and companies with relevant experience in the area of corporate responsibility, as well as screening the issues covered by the media. We also looked at analyses of ESG rating agencies and analysts, proxy advisors and SRI investors, as well as international standards for the management and reporting of corporate policies for sustainable development, such as ISO:26000, GRI, SASB and the Global Compact.

In the second step, to assess the relevance of the identified megatrends, we used the Delphi method, which is based on consolidating the results of several iterative cycles of analysis, conducted with groups of experts. More specifically, we presented the identified megatrends to management and stakeholders, asking them to indicate any additions and prioritize them, taking into account both the potential impact of the megatrends on Generali's activities and the possibility that the Group could influence them, also through the value chain, in line with the double materiality perspective.

Internally, we involved, through interviews and focus groups, more than 120 top managers at Group Head Office and Business Unit level. To ensure adequate consideration of the risk component of the identified mega trends, the internal assessment also incorporated the results of the Group's Own Risk and Solvency Assessment process.

The direct engagement of stakeholders carried out during 2019 involved 50 opinion leaders, selected for their authority and knowledge of the insurance industry or for their ability to provide original and innovative insights. In selecting the stakeholders, we sought adequate representation of all categories of the key Group's stakeholders: retail and corporate customers, suppliers, investors, employees, institutions and regulatory authorities, companies and industry associations, universities and research centres, NGOs and future generations. In the same way, the stakeholder assessment collected with direct engagement was also integrated with desk analysis activities and using artificial intelligence technologies for the quantitative analysis of a large number of documentary sources. In particular, we examined the investment policies of 20 major SRI and traditional investors, the results of demoscopic surveys conducted by Eurobarometer involving a sample of over 114,000 people in Europe and the analysis of a survey conducted with sustainability managers of about 190 multinationals. In addition, through the use of Artificial Intelligence and Computational Linguistics technology, about 1,700 company financial statements, 2,600 regulations and legal initiatives, 4,000 articles published online and over 108 million tweets published between April and October 2019 were analysed.

For the 2020 review following the COVID-19 pandemic, we considered the clients’ opinion gathered through surveys, the most recurring ESG topics covered during engagement with investors and proxy advisors, the assessments from rating agencies and ESG analysts, the main regulatory innovations from European institutions on sustainable finance, and the analyses from think-tanks and international non-governmental organizations.

The combined assessments of internal management and stakeholders resulted in a prioritized distribution of mega trends that was discussed by the Governance and Sustainability Committee and the Board of Statutory Auditors and subsequently approved by the Board of Directors in November 2020.

In the Annual Integrated Report we disclose the measures taken to mitigate risks and seize the opportunities related to the most material mega trends and on the results we have achieved. Indeed, transparency on the Group's responses to these major challenges is an important lever for us to build trust, support stakeholder decision-making and demonstrate our ability to create lasting value.